Top 6 features and benefits of a next-gen SME Loan Origination System

Sep 20, 2024

In India, Small and Medium Enterprises (SMEs) are the backbone of the economy, contributing to about 30% of the country’s overall GDP and employing over 11 crore people. Despite their growing significance in the market, accessing timely finance has been challenging for SMEs. They rely on formal (banks and financial institutions) and informal lending channels to ensure availability of capital. The traditional loan origination systems used by these lenders often leave SMEs waiting for months, unable to keep pace with their evolving requirements and potentially costing them crucial growth opportunities.

This is where the MSME lenders need a next-gen loan origination system to not just meet but also exceed the expectations of today’s promising businesses. For Indian banks and NBFCs, implementing a modern, innovative and customer-centric loan origination system (software platform) is essential to bridge this credit gap.

In this blog, we will:

- Explore the top six features of these advanced loan origination systems.

- Learn how they empower lenders to provide quick and personalized loans.

- Understand how they drive SME and financial institution success by streamlining loan processing, reducing turnaround time and enabling informed lending decisions, thereby saving significant time and resources.

What is a Loan Origination System?

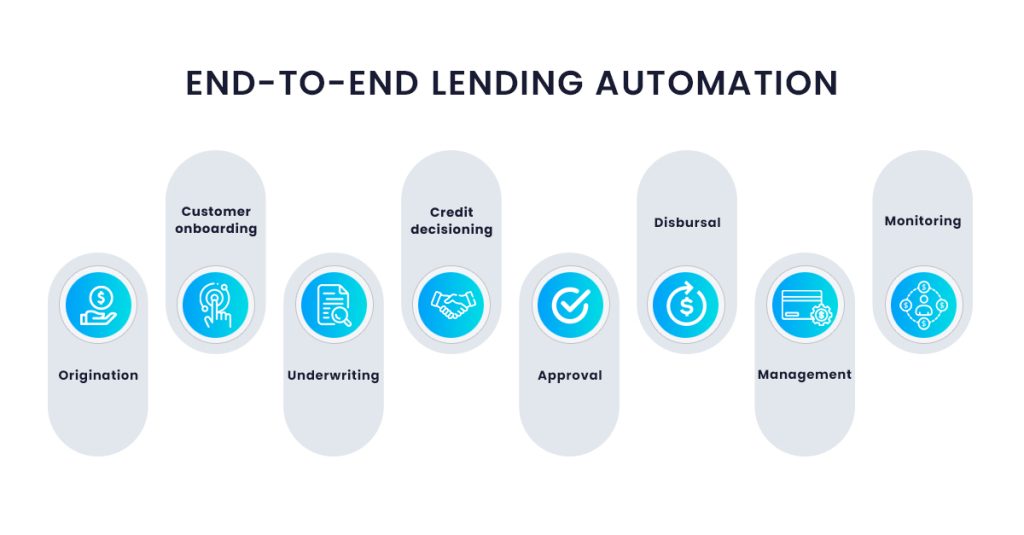

It is a digital platform that automates the entire lending process from loan application and customer onboarding to underwriting, credit decisioning, loan eligibility, approval and disbursal.

A loan origination system benefits banks and financial institutions by saving time, reducing fraud and defaults, increasing operational efficiency, improving borrower relationships and regulatory compliance.

With alternative lenders offering loans within 24-48 hours, banks and financial institutions must adopt innovative digital practices to improve their customer borrowing experiences and remain competitive.

According to a McKinsey report, financial institutions can enhance operational efficiency by 20-30% through digitizing customer journeys and reducing touch time. Moreover, banks and NBFCs can reduce non-performing loan (NPL) risk by 10-25% by making consistent decisions and enhancing risk models. By leveraging a unified, intelligent, comprehensive loan origination system, lenders can disburse loans with higher confidence, while meeting the critical timelines and requirements of today’s SMEs.

A next-gen Loan Origination System goes beyond just fast approvals, it empowers financial institutions to stay ahead of their competition while offering a continuum of value.

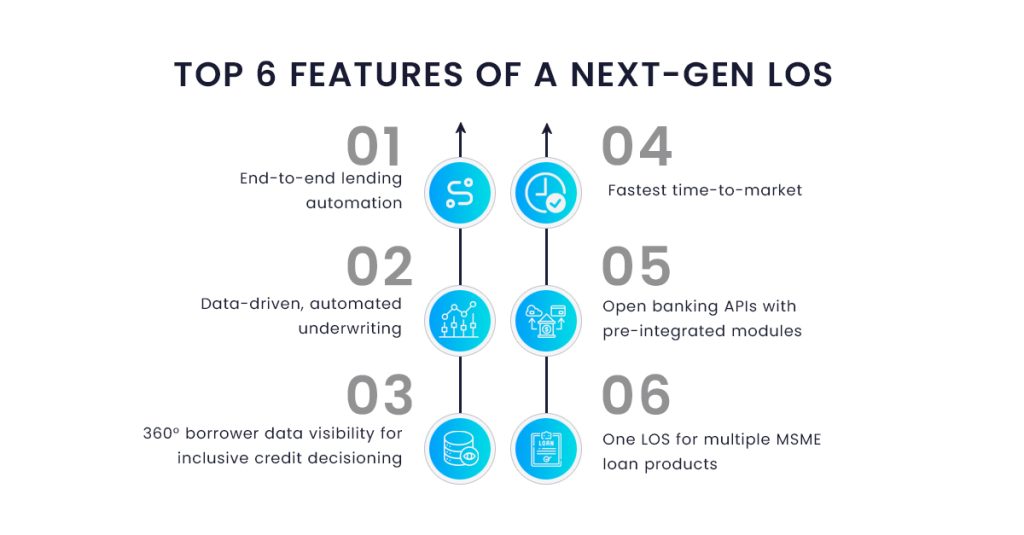

Key features of a next-gen Loan Origination System and their outcomes

1. End-to-end lending automation

The loan origination process, especially In India, is complex, lengthy and plagued by cumbersome manual tasks. A next-gen loan origination system leverages Application Programming Interfaces (APIs) for automated data connectivity and workflows, enabling both lenders and borrowers to continue using their existing systems without any disruption.

Lenders can now scale their operations easily and efficiently handle increased volumes. Automation allows lenders to focus more on serving their customers such as processing Know Your Client (KYC) forms and loan applications, while the software handles their mundane tasks. A cloud-based loan origination system offers adaptable features that seamlessly integrate with existing processes, facilitating a paperless, 24×7 digital lending experience for quicker and accurate credit decision-making and better profitability.

2. Data-driven, automated underwriting

The speed and accuracy of underwriting can significantly impact a lender’s ability to serve its SME customers. Automated underwriting uses data analytics to assess borrower creditworthiness. This is done by analysing data from multiple sources.

It streamlines the lending process with customizable workflows, eligibility criteria, screening procedures and decision-making based on established policies. Additionally, it enables quick classification of loan applicants into risk tiers using rule-based scorecards and multiple application parameters, accelerating loan approvals, rejections or recommendations.

3. Comprehensive borrower insights for better decision making

A 360-degree view of a borrower’s financial health, offered by a loan origination system, is utmost critical for informed lending decisions. AI-driven credit decisioning pulls data from various sources, creates a comprehensive borrower profile, offers insights into market fluctuations and empowers lenders to decide appropriately. Custom controls based on a lender’s business rules can be easily configured. Unlike manual procedures that may take days to finalize, AI-based credit decisioning yields results within minutes, improving efficiency and accuracy.

4. Faster time-to-market

We operate in a digital world today where speed is of the essence, especially when 77% of Indian SMEs still rely on informal credit channels because of the delays that exist in the formal loan approval processes. The long waiting times are now getting replaced by innovation and adaptability.

A next-gen loan origination system enables financial institutions to rapidly develop and deploy new loan products, significantly reducing time-to-market. Developing a new SME loan product or configuring an existing one is now a matter of hours not weeks.

5. Open banking APIs with pre-built modules

Open banking is improving the financial landscape in India and a next-gen loan origination system leverages this trend to its fullest. With open banking, customers can now integrate a range of third-party services, improving credit scores, loan terms, interest rates and budgeting solutions.

This approach improves credit analytics by providing lenders with a comprehensive overview of both traditional and non-traditional customer data, leading to accurate credit decisioning models. A robust loan origination system with third-party integrations not only improves lending outcomes but also drives product innovation and customer-centricity.

6. One LOS for multiple MSME loan products

Given the diverse nature of SME loans in India, managing multiple loan products with different requirements can be extremely challenging. Most lenders use the same application and underwriting processes for all loans, regardless of complexity or borrower profile. This means that the operational expenses of processing a large or a small one are somewhat similar.

A loan origination system with automated workflows customized to various credit types can significantly optimize these costs. It allows quick integration of new loan products quickly while offering a unified platform for customers, employees and partners. By consolidating your lending process and bringing all stakeholders and teams onto a unified platform, you streamline processes, minimize errors, deliver fast and accurate underwriting decisions and improve overall customer satisfaction.

CredAcc’s no-code Loan Origination System for better, faster, and more profitable SME lending

To compete with alternative lending channels and to stay competitive in the complex SME lending arena, Indian banks and NBFCs must use an outside-in approach. By adopting an AI-driven loan origination system like CredAcc, you can now automate many parts of your lending process while enjoying the flexibility to innovate and deploy new-age loan products. With CredAcc’s no-code LOS, lenders get the best of both worlds—combining the flexibility of building with the ease of buying. Our platform allows Banks and NBFCs to customize lending processes, workflows, and decision-making models to fit their business needs—without the long development cycles or high costs. CredAcc enables lenders to launch new products faster, adapt to market changes, and still rely on a secure, scalable infrastructure. This smart, hybrid approach minimizes complexity and costs, keeping lenders competitive and ready to scale efficiently.

The key advantage of being a no-code platform is that it future-proofs your systems and processes against changing technological and market trends. You can scale your operations easily without relying heavily on your IT staff while empowering your loan servicing agents to make on-the-fly changes for incoming cases. AI-driven alerts and nudges, along with advanced automation ensure that case management capabilities and loan processing turnaround times are significantly improved.

CredAcc’s system offers deep subject-matter insights that sets it apart from other commercial players. Considering the economic importance and profitability of SME lending, CredAcc is committed to supporting your digital lending transformation transformation journey with modern, easy-to-use and highly configurable loan origination solutions.

Book a demo to learn more.