Everything you need to know about Business Credit Report

Sep 26, 2024

What is a Business Credit Report?

In simple terms, it is an essential document that outlines a company’s financial stability and creditworthiness. Think of it as a personal credit report but for a business. Such a report would typically include a company’s credit accounts, payment history, outstanding debts and public records such as bankruptcies or liens. Just as a personal credit score affects an individual’s ability to borrow, a business credit report provides lenders, investors, suppliers and partners a comprehensive overview of how well a particular company manages its finances.

This report is crucial for anyone looking to assess a company’s financial health and reliability, before extending credit or entering into a financial agreement. Understanding and managing your business credit reports can be the difference between securing or losing financing with and favourable terms or attracting new business opportunities.

In this blog, we will walk you through the basics of business credit reports, their components, their impact on your business and tips on improving your business credit score.

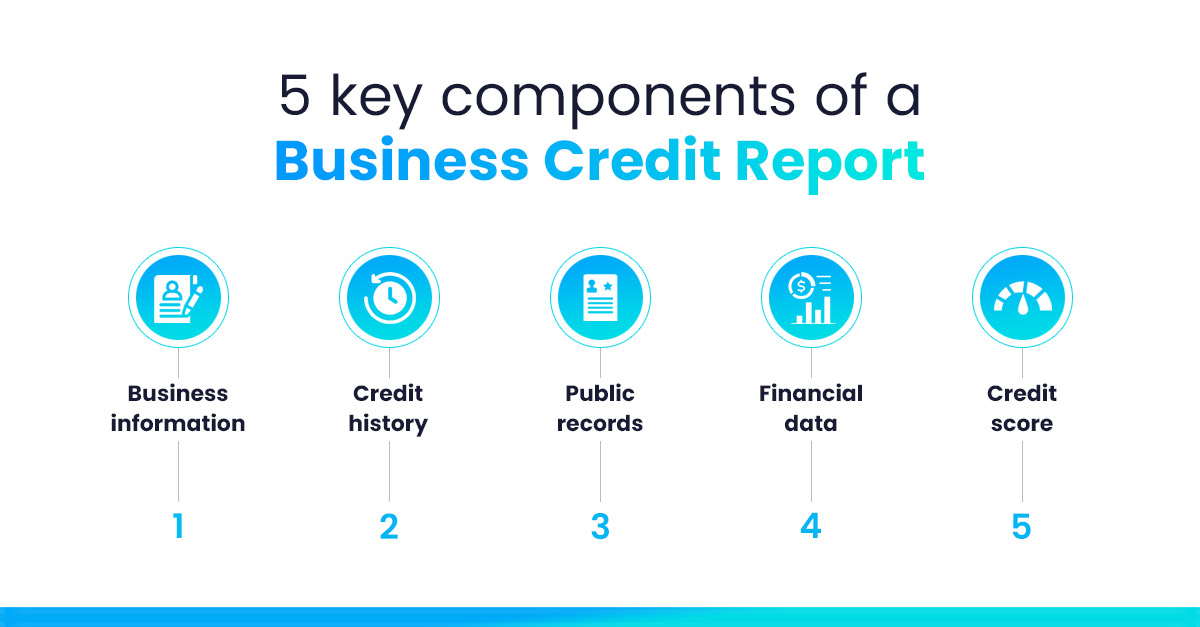

Key components of a Business Credit Report

- Business information: includes company name, address, industry classification and ownership details.

- Credit history: shows credit accounts, payment behaviours and outstanding debts.

- Public records: lists liens, judgments and bankruptcies, providing insights into legal and financial issues.

- Financial data: includes financial statements and other relevant available data for a comprehensive financial analysis.

- Credit score: provides a numerical representation of the company’s credit risk, helping lenders, suppliers and investors make informed lending decisions.

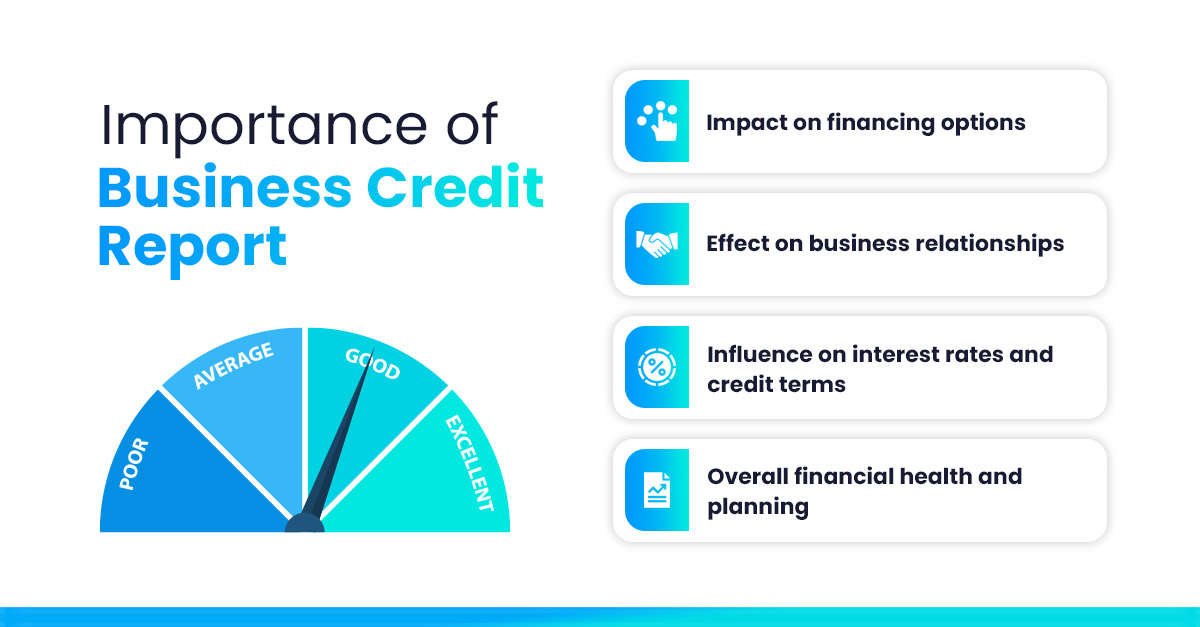

Why is a Business Credit Report important?

1. Impact on financing options

As part of their due diligence, lenders first analyse this report when evaluating loan or credit applications, determining eligibility, amount and terms and conditions of financing. A good business credit report is essential for securing financing with minimal effort and from trusted sources. It indicates your prospective lenders’ confidence in your business’s reliability and stability. A good report, based on a high credit score opens more funding opportunities, while a poor one can severely limit access to the capital you need.

2. Effect on business relationships

Your business credit report significantly impacts relationships with suppliers, partners and even customers. Suppliers might use this report to decide whether to offer trade credit and on what terms. Potential partners may review this report during their due diligence process, influencing negotiations and collaborations.

3. Influence on interest rates and credit terms

A small business credit report directly impacts the cost of borrowing. Small businesses with strong credit reports often enjoy lower interest rates and better credit terms, reducing the overall cost of debt. On the other hand, a lower credit score can lead to higher interest rates, increasing your borrowing cost and affect your cash flow.

4. Overall financial health and planning

It provides a comprehensive overview of your company’s financial position, offering valuable insights for strategic planning and decision-making. Regularly reviewing this report can help you identify strengths and weaknesses, and work on certain areas of improvement. It serves as a roadmap for improving financial performance, ensuring competitiveness and adaptability for future challenges.

Business Credit Score calculation in India

Calculating a business credit score involves several complex factors and varies across credit bureaus and financial institutions. In India, the Credit Information Bureau (India) Limited (CIBIL) through its CIBIL Rank and Commercial CIBIL Score, plays a key role in defining lending scenarios, reflecting upon the unique aspects of the Indian market.

The CIBIL Rank, ranging from 1 to 10, assesses the creditworthiness of commercial entities, with 1 being the highest. The Commercial CIBIL Score for small and medium-sized enterprises (SMEs) ranges from 300 to 900, with a higher score indicating lower risk.

Other prominent credit bureaus like Experian, CRIF High Mark and Equifax also contribute to the business credit scoring landscape in India. Their models consider factors such as credit utilization, payment history and business financial statements, all of which are critical for evaluating a business’s creditworthiness. CRIF High Mark also provides detailed credit reports and scores that encompass a business’s credit activities and repayment history. These models are crucial in facilitating credit lending decisions, helping lenders evaluate the risk associated with lending to businesses in diverse sectors of the Indian economy.

Factors that influence your Business Credit Score

- Payment history: Timely payments demonstrate reliability and improve your credit score, while late payments, defaults or bankruptcies can significantly lower it.

- Credit utilization: This is the amount of credit you are actually using. Lower utilization generally indicates good financial management and improves the credit score.

- Length of credit history: A longer history gives more data points, increasing confidence in the business’s financial background.

- Types of credit accounts: A mix of different credit accounts such as trade credit, loans and lines of credit indicates that your business can effectively manage various types of borrowing.

- Recent credit inquiries: Each time a business applies for credit, a credit inquiry is recorded. Multiple inquiries over a short period can suggest financial distress, potentially lowering the credit score.

How to check your Business Credit Score

To access your score, follow these steps:

- Identify major credit reporting agencies: Research the most-recognized in your region. For example: CIBIL, Equifax, Experian or CRIF High Mark in India. Each agency offers a different view of your credit profile, so it is important to consider reports from multiple sources for a complete picture.

- Set up an account: Visit the credit bureau’s website and create an account by providing business identification information. This may include a fee.

- Request a credit report: Once your account is active, request a copy of your business credit report. Some agencies provide instant digital reports, while others may send you a physical copy.

After receiving your report, carefully review the details. Understand your business credit score, what influences it and check for any discrepancies. If you find any inconsistencies, follow up with the agency to correct it. Knowing how to read these reports is important because provides insights into your business finance and helps you improve your credit score with time.

Tips for improving your Small Business Credit Score

- Pay bills on time: Timely payments improve your credit score. Consider setting up reminders or automating payments to ensure bills are paid on time. This also helps avoid any late fees.

- Reduce outstanding debt: Lowering your debt improves your credit utilization ratio, contributing to your score. Focusing on paying high-interest debts first will help reduce financial burdens on the company as well.

- Establish a long credit history: A long but well-managed credit history is a confidence booster. Maintaining long-standing, mutually beneficial relationships with creditors and lenders will establish a strong and reliable credit lineage for your business.

- Diversify credit accounts: Use software tools and automated systems to avail and manage a variety of credit accounts (trade credit, loans or lines of credit)

Regularly monitor your credit report: Check your small business credit report for errors and discrepancies and promptly address any issues. - Build relationships with credit-reporting vendors and suppliers: Work with vendors and suppliers who report to credit bureaus. Building positive payment relationships with these entities can support your small business credit checks over time.

Common mistakes to avoid with Business Credit Reports

Many businesses are unaware of the potential pitfalls that can negatively impact their ability to secure loans. Let us explore some common mistakes to avoid and ensure your reports reflect your true financial health:

- Ignoring your business credit score: Even though you may have a good credit score, failing to regularly monitor your business credit score can lead to missed opportunities for improvement and undetected errors.

- Mixing personal and business finances: This can blur the lines of your small business credit profile and complicate financial assessments.

- Applying for too much credit quickly: A rookie mistake, many loan applications in a short time frame can signal financial trouble, set red flags for your creditors and potentially lower your credit score.

-

Not monitoring your credit report regularly: This can result in inaccuracies that affect your creditworthiness.

How to dispute errors in your Business Credit Report

- Identify errors: Review small business credit report for errors such as incorrect payment histories, account balances or personal information.

- Contact the credit reporting agency: Reach out to the credit reporting agency where the error appears. Most agencies offer online portals or customer service numbers for resolving disputes.

- Provide documentation: Submit any supporting documentation such as payment receipts, correspondence with creditors or relevant legal documents, to prove the error.

- Follow up: Keep track of communications with the credit reporting agency and persistently follow up until the error gets rectified.

Tools and resources for managing your Business Credit

Managing business credit effectively requires you to be well-informed and proactive. Here are some tools and resources that can assist you:

- Credit monitoring services: These services keep alert you on changes and updates in your credit report and score, enabling you to catch and resolve any potential issues early.

- Financial management software: These tools help you maintain accurate records of income, expenses and debt repayments, which are crucial for healthy credit management. They often include features for budgeting, financial reporting and tax preparation.

- Professional financial advisors: Good financial advisors can provide personalized advice to improve your business credit score. These professionals can help strategize debt repayment, optimize credit usage and improve overall financial strategies.

How CredAcc Credit Control helps businesses with automated underwriting

High-quality business credit reports are the foundation for shaping a company’s financial outlook. These reports influence everything from loan approvals to supplier. For businesses on a rapid growth trajectory, improving their credit posture and offering a comprehensive and accurate business credit report is important. A good business credit report is your clear differentiator during volatile markets and tough economic environments.

CredAcc Credit Control offers an innovative and user-friendly platform that empowers businesses to evaluate distributors, dealers, vendors, suppliers and other counterparties more effectively. It facilitates comprehensive assessments, setting appropriate limits, determining business volumes and seamlessly managing upfront evaluations, monitoring and renewals with next-generation underwriting software. CredAcc Credit Control integrates with bureau credit reports, digital bank statement analysers, automated financial statements and monthly purchase ledger analyses, for faster, data-driven and accurate underwriting.

Book a demo to see how CredAcc can help your business fast-track credit assessments.

Related Resources

Open Banking for SMB Lenders

Feb 16, 2023

Read

#NextGenCreditDecisioning Part 1

Jan 23, 2023

Read